Accept crypto with CoinGate

Accept crypto with confidence using everything you need in one platform.

CBDCs vs Stablecoins — Which Will Prevail? Conclusion (Pt. 4)

As the global financial landscape shifts toward digital money, one debate continues to dominate: central bank digital currencies (CBDCs) or stablecoins – which will define the future?

This four-part series has explored the rise of both models, unpacking their technical foundations, regulatory outlooks, and real-world adoption. Now, in the final chapter, we bring it all together.

If you missed the earlier parts, we recommend starting from the beginning — Part 1, Part 2, and Part 3 — to understand the full picture of how CBDCs and stablecoins are shaping up as the new pillars of digital finance.

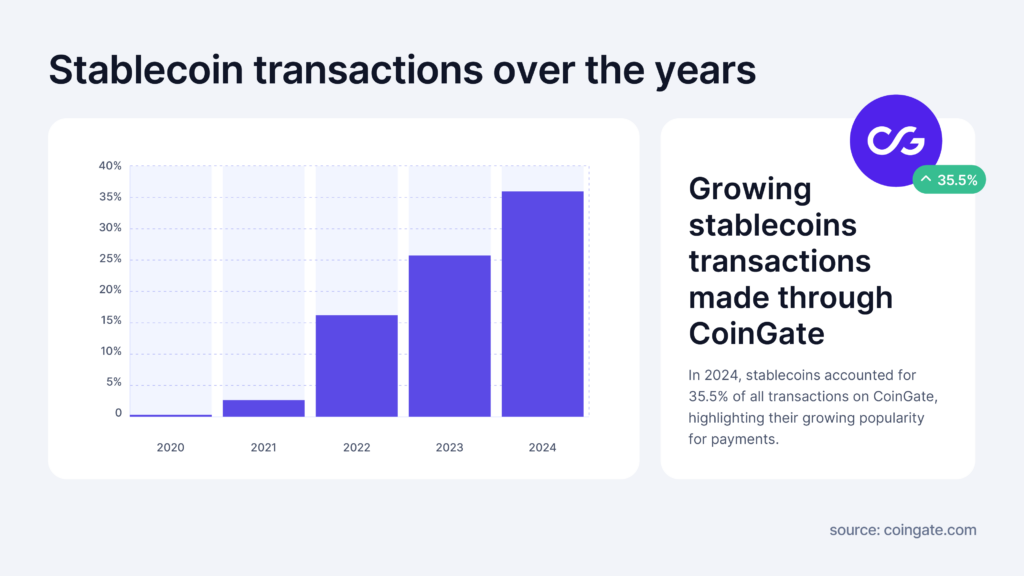

Stablecoins are already being used daily by millions — including in over a third of all transactions processed through CoinGate in 2024 — while CBDCs remain largely in the planning or pilot phase.

At the same time, public opinion, political sentiment, and institutional strategies are shaping the path ahead.

In this conclusion, we’ll assess where each stands, what their strengths and weaknesses are, and whether they’re destined to compete, coexist, or converge. For businesses and individuals navigating this shift, understanding the bigger picture is key.

Let’s dive into the trends, data, and implications to answer the big question: which will prevail – and what should we be doing about it today?

Want to start using stablecoins in your business? Start by signing up for a CoinGate account.

Growing Use of Stablecoins for Payments

As highlighted earlier, stablecoins are no longer just tools for crypto trading; they are becoming a payment medium for businesses and individuals. The data from CoinGate – stablecoins making up 35.5% of transactions in 2024 – is telling.

This suggests that a significant chunk of people who choose to pay with crypto prefer a stablecoin (likely because neither the payer nor the receiver wants value to swing during the payment). Bitcoin, while still widely used, has seen its share of payment transactions drop as stablecoins rise.

We also see new merchant categories embracing stablecoins: freelancers, exporters in developing countries, even some retail stores in crypto-friendly locales now list stablecoin payment options.

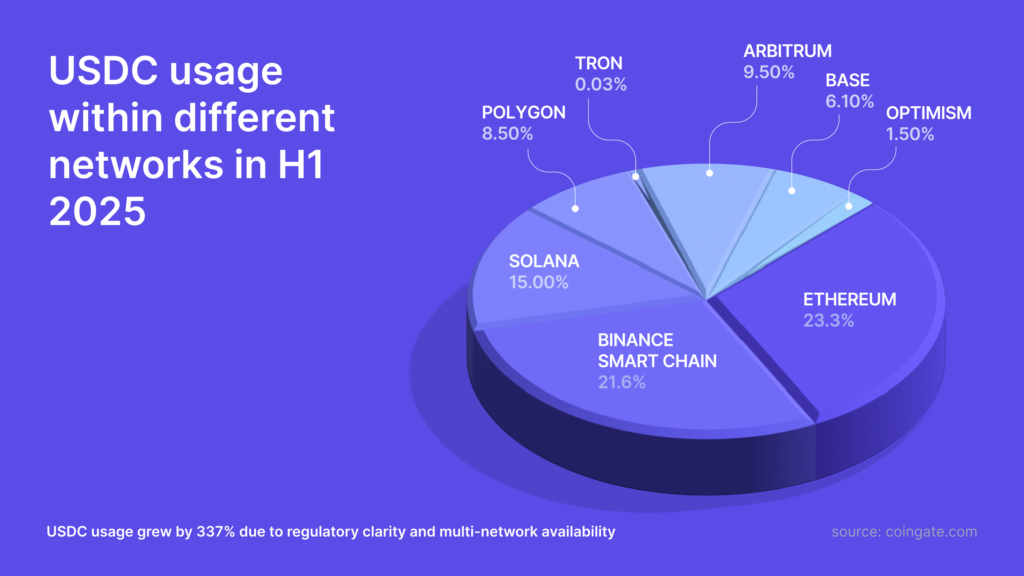

The user experience of paying with a stablecoin is improving too, with Layer-2 solutions and alternative blockchains reducing fees. For instance, many stablecoin users have migrated to the Arbitrum or Base network for near-zero fee USDC transfers, which has made micro-transactions feasible.

As stablecoin payments become routine, people naturally question: if we can do this with a private token today, what added value will a government CBDC bring? This doesn’t mean CBDCs have no place, but it raises the bar for what they must offer to displace or outperform stablecoins.

Public Sentiment Against CBDCs

Over the last two years, awareness of CBDC concepts has increased, and with it, skepticism has been vocalized by parts of the public, tech experts, and politicians (especially in liberal democracies).

The concerns we detailed (privacy, control, etc.) have translated into tangible public opinion trends. For example, in the United States a broad survey found that twice as many Americans oppose a CBDC as those who support it (34% oppose vs 16% in favor), with the rest undecided.

More strikingly, when specific potential features of a CBDC are mentioned, opposition skyrockets – 74% oppose if it would allow the government to control spending, 68% if it allows surveillance of spending. These are overwhelming majorities against the “worst-case” use of CBDC power.

Politicians have picked up on this sentiment; by late 2023 in the U.S., a bill nicknamed the “CBDC Anti-Surveillance Act” even passed the House of Representatives, aiming to block the Federal Reserve from issuing any CBDC that could be used for mass surveillance.

While that bill’s future was uncertain, it signaled strong political resistance. In Europe, public consultation feedback to the ECB showed privacy was the top concern, and as noted, UK parliamentary committees openly questioned the need for a digital pound. Civil liberties groups and privacy organizations have also started campaigns to ensure CBDCs, if created, have ironclad privacy guarantees.

This public pressure means that any CBDC rollout will likely be more restrictive in scope (perhaps limiting data collection, or rolling out gradually) than the theoretical technology would allow. In contrast, stablecoins have not triggered the same public backlash – likely because they are voluntary, user-driven, and not seen as an instrument of state power.

People who don’t trust or want them can simply ignore them, and those who find them useful can opt in. This dynamic is fundamentally different from a government pushing a new form of money to everyone.

Institutional and Corporate Adoption

Another angle in “who prevails” is what large institutions do.

Here we see interesting developments: some major financial institutions and corporations are leaning into stablecoins. For instance, payment networks like Visa have piloted using USDC stablecoin for settling transactions on their network, and there are discussions of integrating stablecoins into card payment flows.

Several banks have explored issuing their own stablecoins or tokenized deposits to facilitate faster clearing. On the other hand, central banks and governments are the only entities that can launch CBDCs, and they move slower. So in the next few years, we are likely to see more real-world business use-cases built on stablecoins (for example, supply chain payments using stablecoins, or fintech apps offering stablecoin wallets for cross-border payments), because the private sector is free to innovate there.

Meanwhile, CBDCs might still be in pilot stage or limited-scope trials (like a city-wide test). First-mover advantage currently belongs to stablecoins. If they can solve problems effectively, they might reduce the demand or urgency for a CBDC.

Coexistence or Competition?

It’s not necessarily a zero-sum game of stablecoin versus CBDC.

Many experts foresee a world where both exist. However, there is certainly a degree of competition: a widely adopted CBDC could reduce the need for private stablecoins (why use USDC if a convenient digital dollar from the Fed exists?), and conversely, entrenched stablecoin usage could make a CBDC redundant (“everyone’s already using digital dollars via stablecoins, so why introduce a new one?”).

Public sentiment will influence this. If people are comfortable with private solutions and wary of government ones, stablecoins will have the edge. Central banks might then adjust by making their CBDCs more palatable (or even choose not to issue one).

We already see central banks taking note of stablecoin success – for example, some proposals involve letting regulated stablecoins be part of the CBDC ecosystem (like having commercial banks issue “stablecoins” that are fully backed by central bank reserves, effectively a synthetic CBDC). This hybrid approach could blur the line between the two concepts in the future.

Which will prevail?

The answer might differ by jurisdiction and use-case. In a country like China with a tightly controlled financial system, the state-backed CBDC (e-CNY) will likely dominate domestically while private crypto is banned – a clear win for the CBDC model (albeit in an authoritarian context).

In the U.S. and much of Europe, if current trends hold, privately issued stablecoins may continue to flourish for years before a retail CBDC ever appears – and that head start could cement their role, especially if they integrate with traditional finance.

Unless a CBDC offers something dramatically better (e.g. universally accepted legal tender digital cash with absolute privacy guaranteed by law), people and businesses might ask: why switch from stablecoins we know and use, to a new app or system?

From a business perspective, what matters is pragmatism and choice. Right now, stablecoins are a practical tool for commerce and transactions, whereas CBDCs are largely theoretical or limited pilots.

Companies can today leverage stablecoins to expand payment options or streamline international settlements. That’s why CoinGate has embraced stablecoins, enabling merchants to accept USDC and other stablecoins easily – it’s about meeting the demand that exists now.

Should CBDCs come to fruition and gain adoption, one can expect payment processors to integrate those as well. But there’s no need for businesses to wait; the existing crypto infrastructure can deliver many benefits already.

Embracing the Future of Digital Money

The contest between CBDCs and stablecoins is often framed as a rivalry, but in practice, the future of digital money might include both – each finding its own niche.

Stablecoins have carved out a critical role by providing what users and businesses needed immediately: a stable digital currency that operates on global crypto rails. They have shown that private innovation can extend the functionality of traditional money across borders and platforms.

CBDCs, backed by central banks, carry the weight of officialdom and could ensure that the benefits of digital currency are accessible to all in a sovereign and secure way, albeit at the cost of moving more slowly and deliberately.

For crypto-curious businesses and individuals, the key takeaway is to stay informed and flexible. Stablecoins are here now and can be leveraged to improve how you transact. If you’re a business, you don’t have to wait for a central bank’s digital currency to offer customers a digital payment option – you can start accepting stablecoins today.

In 2024, over one-third of CoinGate’s processed payments were in stablecoins, underlining that many shoppers are already choosing this method. Adopting stablecoins via a trusted gateway can also future-proof your business for a world where digital currencies (of one type or another) become the norm.

On the other hand, it’s wise to watch developments in the CBDC space. Especially in regions like the EU, a digital euro could become a reality in a few years. Governments will likely roll out extensive information campaigns and infrastructure when the time comes.

If CBDCs are implemented with the promised privacy and convenience features, they could achieve widespread usage – potentially becoming an official, no-counterparty-risk complement to private payment options.

At that point, businesses will want to integrate CBDC acceptance (much like accepting another form of fiat, just in digital guise). The good news is that the same technology enabling crypto payments could be adapted for CBDCs if they use similar standards.

In conclusion, will CBDCs or stablecoins prevail? The most realistic scenario is coexistence, at least for a significant period.

Stablecoins have the first-mover advantage and the momentum right now, especially in the open cryptocurrency markets and as cross-border payment tools. CBDCs have the institutional backing and could leverage legal tender status to gain ground, particularly for domestic offline payments and inclusion efforts by governments.

Public opinion will heavily influence this balance: if people reject the notion of a government-run digital currency, stablecoins (and good old cash) may keep dominating the public’s preference. If, conversely, central banks manage to deliver CBDCs that citizens find useful and trustworthy, we could see a gradual migration to those for everyday transactions, with stablecoins perhaps continuing to serve specialized roles (like inter-exchange transfers, DeFi, etc.).

One thing is clear – the world is moving toward digital currency in one form or another. For businesses and individuals, the smart approach is to engage with these technologies early and thoughtfully.

Stablecoins already offer a gateway into this new financial era, and they are bridging the gap to whatever comes next.

CoinGate, for example, is at the forefront of this bridge, helping thousands of businesses transact in stablecoins and other cryptocurrencies effortlessly. By embracing such solutions, you’re not only benefiting from current technology but also positioning yourself advantageously for a future where digital money (be it a stablecoin or a CBDC) is commonplace. Ready to start? Sign up for a CoinGate account.

The evolution is ongoing. Stay informed, remain adaptable, and leverage the tools that make sense today. In the end, whether it’s a CBDC or a stablecoin that “prevails” in usage, the goal for all of us is a smoother, more inclusive, and innovative financial system.

Both of these digital currency models are steps toward that goal. And with a balanced approach, we can reap the benefits while managing the risks – ensuring that the future of money truly serves the needs of businesses and individuals in the digital age.

Accept crypto with CoinGate

Accept crypto with confidence using everything you need in one platform.