Accept crypto with CoinGate

Accept crypto with confidence using everything you need in one platform.

Crypto Payouts vs. SWIFT Transfers: Cost and Speed Comparison

Cross-border payments remain one of the most persistent friction points for businesses operating internationally. If you are settling supplier invoices in Southeast Asia, compensating contractors across the European Union, or distributing revenue shares to global partners, the payment method you choose directly affects your bottom line – and your operational efficiency.

For decades, the SWIFT network has been the default rail for cross-border business transfers. It is a system that works, connecting over 11,000 financial institutions across 200+ countries. But it comes at a cost – in both money and time – that a growing number of companies now find difficult to justify, especially when making frequent or high-volume international payments.

Think it’s time to introduce cryptocurrency operations to your business? Sign up for CoinGate.

Crypto payouts, powered by blockchain infrastructure, present a fundamentally different model: direct transfers without intermediary banks, settlement in minutes rather than days, and transparent fees that are a fraction of traditional wire costs. But how do these two systems actually compare when evaluated against the demands of real business operations?

This guide provides a detailed, side-by-side analysis of crypto payouts and SWIFT transfers across the dimensions that matter most to finance and operations teams: cost, speed, global reach, compliance, and scalability. The goal is not to declare one system universally superior, but to give you the data you need to determine which approach – or which combination – best fits your specific operational profile.

How SWIFT Transfers Work – And Where They Fall Short

SWIFT (Society for Worldwide Interbank Financial Telecommunication) is not a payment system in itself – it is a messaging network that facilitates payment instructions between banks. When you initiate a SWIFT transfer, your bank does not send money directly to the recipient’s bank. Instead, it sends a secure message through the SWIFT network, instructing a chain of correspondent banks to relay the funds.

The Correspondent Banking Chain

A typical SWIFT transfer follows this multi-step path:

- Your bank (the originating bank) receives the payment instruction and debits your account.

- If your bank does not have a direct relationship with the recipient’s bank, it routes the payment through one or more correspondent (intermediary) banks that serve as bridges between the two institutions.

- Each intermediary bank in the chain processes the payment, applies its own fees, performs its own compliance checks, and passes the instruction forward.

- The recipient’s bank (the beneficiary bank) finally credits the funds to the recipient’s account – typically 3 to 5 business days after the transfer was initiated.

The number of intermediaries depends on the banking corridor. A transfer from a major European bank to a US institution may pass through one intermediary. A transfer to a bank in a smaller market – say, from Lithuania to the Philippines – may involve two or three, with each adding latency and cost.

The Real Cost of SWIFT for Businesses

According to the World Bank’s Remittance Prices Worldwide database, the global average cost of sending money internationally remains above 6% for smaller amounts. For business-scale transfers, the fee structure is complex and often opaque:

- Sending bank fees: $25–$50 per transfer, depending on the bank and account type.

- Intermediary bank fees: $15–$30 per intermediary hop. Most transfers involve at least one intermediary; some involve two or three.

- Receiving bank fees: $10–$25, often deducted from the transferred amount so the recipient receives less than expected.

- FX markup: Banks typically apply a 0.5%–3% spread above the mid-market exchange rate, which is often not disclosed transparently.

- Total effective cost: $50–$120+ per international wire, depending on corridor and intermediaries involved.

For a business making 100 international payouts per month, that translates to $5,000–$12,000 in monthly transfer fees alone – before factoring in the administrative time to initiate, track, and reconcile each payment. At 500 payouts per month, the cost balloons to $25,000–$60,000. These are not theoretical figures; they are the operational reality for companies that rely on SWIFT for regular cross-border disbursements.

The Time Cost: Business Days Only

SWIFT operates on banking hours. Transfers initiated on a Friday afternoon may not begin processing until Monday. Add in time zone differences, compliance holds at intermediary banks, and local banking holidays, and a “3–5 business day” estimate can easily stretch to a week or more for certain corridors. For businesses that need to meet contractual payment deadlines or maintain partner trust, this unpredictability is a significant operational risk.

How Crypto Payouts Work – A Direct Alternative

Crypto payouts use blockchain networks to transfer value directly from sender to recipient, eliminating the need for intermediary banks entirely. The sender initiates a transaction – either manually from a wallet or programmatically through a payment platform – and the blockchain network validates and settles it, typically within minutes.

Key Mechanics of Blockchain Payouts

- No correspondent banks. Funds move peer-to-peer on-chain. The transaction goes from sender’s address to recipient’s address with no intermediary processing steps.

- Settlement in minutes, not days. Bitcoin transactions typically confirm within 10–60 minutes. Stablecoins on networks like Tron (TRC-20) or Solana often settle in under 10 seconds. Layer 2 solutions on Ethereum bring settlement times to seconds as well.

- Transparent, predictable fees. Network fees are published and typically range from $0.01 to $5, depending on the blockchain and current network congestion. These are the base network fees only – regulated payout platforms charge additional service fees (e.g., CoinGate charges 0.50 EUR + 0.5% per payout). Even with platform fees included, the total cost remains a fraction of SWIFT. Critically, network fees are the same whether you are sending $100 or $100,000 – they scale with the transaction’s data size, not its monetary value. See the full pricing.

- 24/7/365 availability. Blockchain networks do not observe banking hours, weekends, or holidays. A payout initiated at 11 PM on a Sunday settles just as quickly as one sent on a Tuesday morning.

- Global reach without banking infrastructure. Recipients need only a compatible wallet address – available as a free mobile or desktop application. No bank account, no SWIFT/BIC code, no receiving bank approval process.

From P2P to Payout Platform (Why Infrastructure Matters)

While peer-to-peer blockchain transfers deliver clear advantages over SWIFT in speed and cost, they have practical limitations for business use. Manual P2P transfers require managing individual wallet transactions, offer no built-in compliance or audit trails, and provide no FX conversion, batch processing, or role-based approval workflows. For a one-off payment, P2P works fine. For regular, high-volume business payouts – where compliance, scalability, and operational control are non-negotiable – purpose-built payout infrastructure is the practical choice.

Platforms like CoinGate retain the core blockchain advantages – speed, global reach, low base network fees – while adding the business-grade features that finance teams require: automated FX conversion, CSV and API-based batch processing, comprehensive transaction records, and full regulatory compliance. This infrastructure is not free, but these costs remain dramatically lower than traditional banking at scale, and you gain compliance, automation, and auditability that raw P2P transfers cannot provide.

Stablecoins: Removing the Volatility Objection

Historically, the most common objection to crypto-based business payments was price volatility. Sending a $5,000 payout in Bitcoin that arrives worth $4,700 (or $5,400) is unacceptable for routine business operations.

Stablecoins have effectively solved this problem. USDC (USD Coin), for example, is pegged 1:1 to the US dollar and backed by fully reserved assets. When you send $5,000 in USDC, the recipient receives exactly $5,000 in value – regardless of what Bitcoin or Ethereum markets are doing.

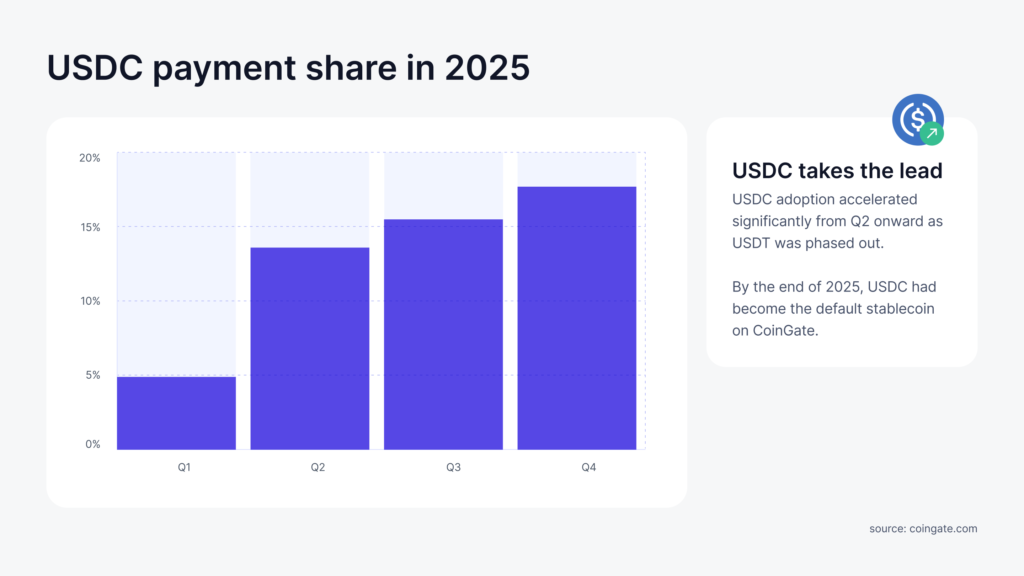

The adoption trajectory reflects this utility. In 2025, stablecoins accounted for nearly 30% of all payments processed through CoinGate, with USDC growing over 1,264% year-over-year – driven in part by the regulatory clarity that MiCA brought to the European stablecoin market.

For businesses evaluating crypto payouts, stablecoins represent the practical entry point: blockchain speed and costs, with fiat-equivalent stability.

Head-to-Head Comparison: Crypto Payouts vs. SWIFT Transfers

| Factor | SWIFT Transfer | Crypto Payout |

| Transaction fee | $50–$120+ per transfer | $0.01–$5 (blockchain network fee) |

| Settlement time | 3–5 business days (often longer) | Minutes (often seconds for stablecoins) |

| Operating hours | Business hours only, Mon–Fri | 24/7/365, no downtime |

| Intermediaries | 1–3 correspondent banks | None – direct peer-to-peer |

| FX transparency | Hidden markups on exchange rates | Transparent on-chain conversion rates |

| Recipient requirements | Bank account + SWIFT/BIC codes | Wallet address only (free to create) |

| Audit trail | Statement-based, delayed availability | On-chain TXID, verifiable in real-time |

| Scalability for batches | Each payment processed individually | Batch processing via CSV or API |

What the Numbers Mean at Scale

The cost differential is particularly dramatic for businesses making frequent international payments. Consider this scenario: a company sends 500 payouts per month to international partners, contractors, and suppliers. At an average SWIFT cost of $75 per transfer (conservative, considering intermediary fees and FX markup), the annual cost is $450,000 in transfer fees alone. The same 500 payouts via stablecoin transfers on a low-cost blockchain network would cost under $2,500 annually in network fees – even accounting for platform fees from a regulated payout provider.

That is not a marginal improvement. It is a structural cost reduction that directly impacts operating margins – and it becomes more pronounced as payout volume increases.

When SWIFT Still Makes Sense

Despite the advantages of crypto payouts, SWIFT transfers remain the better option in certain scenarios. A balanced evaluation should acknowledge these:

- Large fiat-to-fiat corporate transactions: Major acquisitions, real estate closings, or institutional-scale transfers where both parties operate exclusively in traditional banking and the per-transaction fee is immaterial relative to the transfer amount.

- Counterparties unable or unwilling to receive crypto: Some suppliers, particularly in heavily regulated sectors (e.g., government contractors), may not have the infrastructure or authorization to accept digital assets.

- Jurisdictions with restrictive crypto regulations: A small number of countries have outright bans or significant restrictions on cryptocurrency transactions. For payouts to recipients in these regions, traditional banking remains the only viable option.

However, the direction of travel is clear. The regulatory landscape is maturing rapidly, recipient familiarity with crypto wallets is increasing, and the cost-speed-reach equation favors blockchain rails for an expanding range of business payment scenarios.

Compliance and Regulatory Maturity

Perhaps the most significant development in crypto payouts over the past two years has been regulatory maturity. The question is no longer “Is this legal?” but rather “Is the provider I am using properly licensed and compliant?”

The EU’s Markets in Crypto-Assets (MiCA) regulation, fully implemented in 2025, established comprehensive rules for crypto-asset service providers across all 27 EU member states. This created a clear regulatory framework that businesses can rely on – and that licensed providers like CoinGate operate within.

What does compliance look like in practice for crypto payouts? Regulated platforms provide:

- Full AML (Anti-Money Laundering) and KYC/KYB (Know Your Customer / Know Your Business) screening

- Transaction monitoring and suspicious activity reporting

- Comprehensive audit trails with TXID, timestamps, fee breakdowns, and FX conversion data

- Role-based access controls with multi-factor authentication

- Exportable reports designed for tax, accounting, and regulatory filings

When evaluating a crypto payout provider, verify their regulatory status, review their compliance documentation, and confirm they offer the governance controls your finance and compliance teams require. The distinction between licensed and unlicensed crypto processors is significant – and choosing a regulated provider protects your business from counterparty risk.

How CoinGate Enables Compliant Crypto Payouts at Scale

CoinGate’s crypto payouts platform is purpose-built for businesses that need to move funds globally with speed, transparency, and regulatory compliance. Operating under both a MiCA license and Payment Institution authorization in the EU, the platform offers three distinct payout workflows to match different operational needs:

Dashboard Payouts – Quick, Manual Transfers

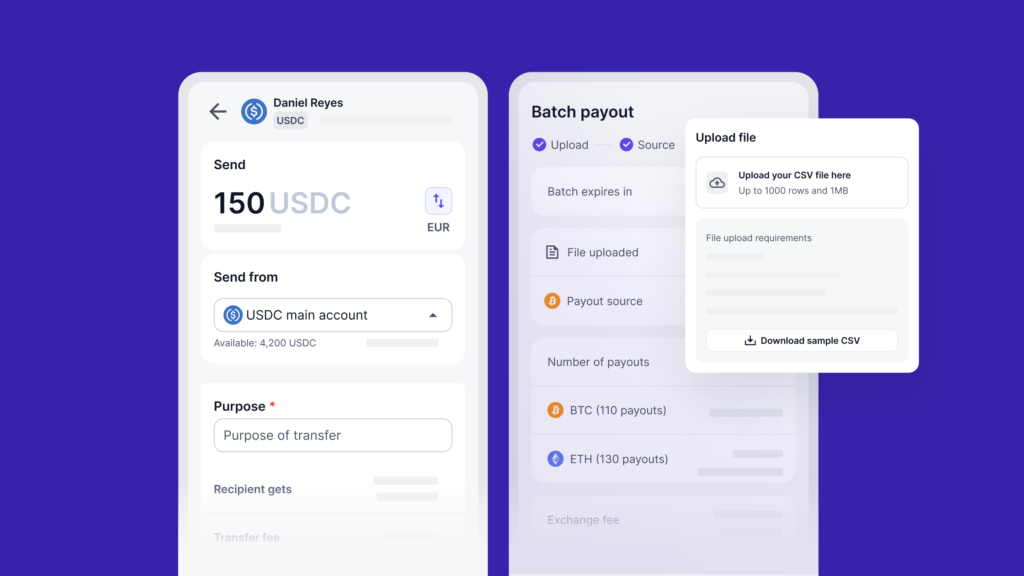

Log into your CoinGate account and send one-off payments to vendors, suppliers, or contractors directly from the dashboard interface. This method requires no integration or technical setup – you simply select the recipient, choose your source balance, enter the amount, and confirm. It is ideal for ad-hoc payments or businesses just beginning to use crypto for disbursements.

CSV Batch Payouts – Scale Without Code

Upload a CSV file containing recipient wallet addresses, preferred cryptocurrencies, network selections, and payment amounts. CoinGate validates all fields automatically, performs any required FX conversion, and processes the entire batch in a single operation. This approach is ideal for periodic payout cycles – monthly affiliate settlements, quarterly partner distributions, or bi-weekly contractor payments – and requires no engineering resources to implement.

API Automation – Full Programmatic Control

For businesses running continuous or high-frequency payout operations, the CoinGate Payouts API enables complete automation. Connect directly with existing back-office systems, trigger payouts programmatically based on business logic, pay in any supported asset based on fiat values using a single API call, and monitor the full payout lifecycle via webhooks. This is the approach used by the majority of CoinGate’s business clients – 85% of merchants automate payouts via API.

Built-In FX Conversion

CoinGate’s FX payout feature allows you to hold one asset – whether EUR, BTC, USDC, or any other supported currency – and deliver payouts in a different cryptocurrency of the recipient’s choice. The conversion happens automatically at the moment of payout execution. FX payouts are charged at 0.50 EUR + 1.5% per transaction – transparent and predictable, with no hidden markups (see coingate.com/pricing). This means you do not need to maintain balances in multiple currencies or perform manual conversions before each payout cycle.

Enterprise Governance and Compliance

Every payout through CoinGate is backed by transparent records including TXID, timestamps, network fees, and FX conversion data. Role-based permissions allow you to separate payout initiators from approvers, activity logs provide full auditability, and all records can be exported for seamless integration with your accounting and compliance workflows.

Making the Right Choice for Your Business

SWIFT is not going away. For certain use cases – particularly large, infrequent fiat-to-fiat transfers between established banking relationships – it remains a practical choice. But for businesses that make frequent international payments, the comparison increasingly favors crypto rails.

The decision ultimately depends on your operational profile:

- Low-volume, fiat-only operations with traditional banking counterparties – SWIFT remains the path of least resistance.

- High-volume, international, multi-currency operations – Crypto payouts deliver measurable cost reduction, faster settlement, broader geographic reach, and cleaner reconciliation.

- Mixed operational profile – A hybrid approach – using SWIFT for legacy banking relationships while shifting an increasing share of cross-border payouts to crypto rails – is how many businesses are managing the transition.

The businesses that evaluate both options objectively and adopt the right tool for each use case will operate leaner and faster than those that default to the status quo. The data supports the shift. The regulation enables it. The infrastructure is ready.

Ready to reduce your cross-border payment costs? Explore CoinGate’s crypto payouts or create a free account to send your first payout today.

Accept crypto with CoinGate

Accept crypto with confidence using everything you need in one platform.