Accept crypto with CoinGate

Accept crypto with confidence using everything you need in one platform.

VAT and Tax on Accepting Crypto Payments: What EU Businesses Need to Know

There’s a myth that won’t die. “Crypto is untaxed, so if I get paid in it, the taxman looks the other way.”

He does not.

Accepting crypto changes how the money moves. It doesn’t change whether you owe VAT or tax on the sale. VAT on crypto payments follows the rules it always followed. If anything, they’re clearer than most business owners expect, and getting them right is mostly about record-keeping rather than anything exotic.

Before we go further, one honest caveat. This is general information, not tax advice, and crypto tax treatment differs across all 27 EU member states. Treat what follows as a map of the terrain, then check the details with a qualified local advisor before you file anything.

Want the payment records your accountant will ask for? Start accepting crypto with CoinGate.

The ruling everyone half-remembers: Hedqvist

Most crypto tax conversations eventually reach the same landmark case, usually mangled. So let’s state it correctly.

On 22 October 2015 the Court of Justice of the EU decided Skatteverket v Hedqvist (Case C-264/14). It made two findings. Exchanging traditional currency for Bitcoin, and back again, is a supply of services for consideration under Article 2(1)(c) of the VAT Directive. And that supply is exempt from VAT under Article 135(1)(e), the exemption covering transactions concerning currency, banknotes and coins used as legal tender.

That’s the part people half-remember. Here’s the part they forget: the ruling only covered the exchange transaction itself. It said nothing about selling goods or services that happen to be paid for in crypto. It didn’t touch income tax, corporate tax, or capital gains. It was about swapping money for Bitcoin, and nothing more.

Which brings us to the distinction that actually matters for a business.

Getting paid in crypto does not remove VAT on your sale

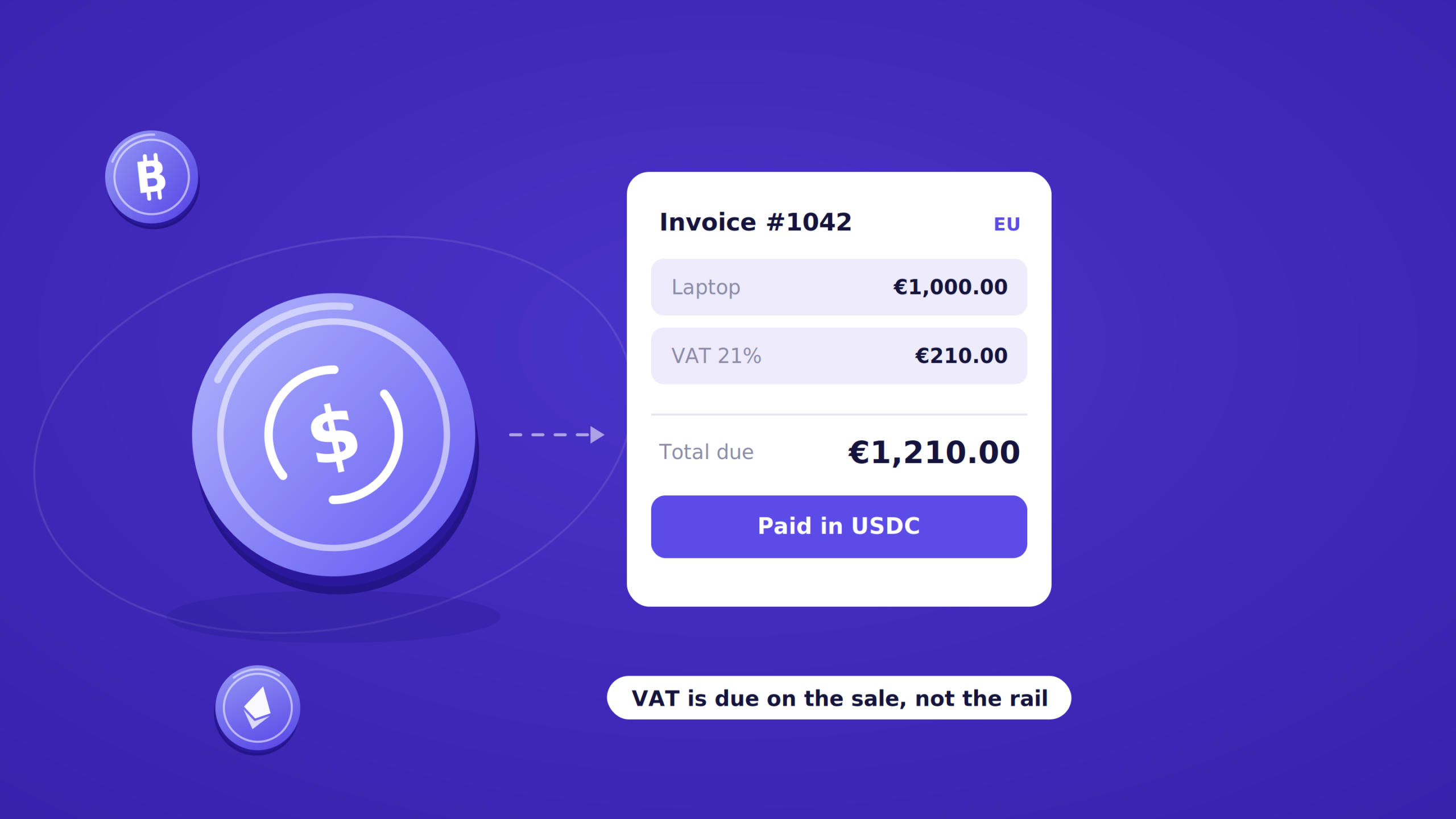

Here’s the rule in one line. If you sell something that’s subject to VAT, it stays subject to VAT no matter what the customer pays with.

Crypto is just the payment method. A customer paying you in USDC is treated the same as a customer handing you a card or a bank transfer. The VAT is due on the underlying goods or services, at the same rate, exactly as before.

So if you sell a 1,000-euro laptop and the customer pays the equivalent in crypto, VAT is due on 1,000 euros. The crypto didn’t make the sale tax-free. It just settled the bill.

Which value, at which moment?

If VAT is due on the sale, the next question is obvious. What number do you put on the invoice when the customer paid in a token that swings in price?

Express the taxable amount in your accounting currency, using the crypto’s fiat value at the time of the transaction. You’re charging VAT on the euro value of what you sold, not on a nominal crypto figure. Irish Revenue puts it plainly: the taxable amount for VAT purposes is the euro value of the cryptocurrency at the time of the supply.

Which rate, though? Crypto is not a foreign currency, so no article of the VAT Directive was written with it in mind. The mechanism tax authorities reach for anyway is Article 91(2), the rule for converting foreign-currency amounts: the most recent selling rate on the representative exchange market at the moment VAT becomes chargeable, or the latest rate published by the European Central Bank. Germany says so explicitly, applying Article 91(2) by analogy and accepting the last published selling rate from a conversion portal, as long as you document which rate you used.

So the shape of the rule is known, and it works much like foreign-currency invoicing. What varies is which rate source your own tax authority will accept, and how strictly it reads “at the moment”. That’s a confirm-with-your-advisor point, not a trust-a-blog point.

The income and corporate tax layer

VAT is only one side. There’s also the tax on the income itself.

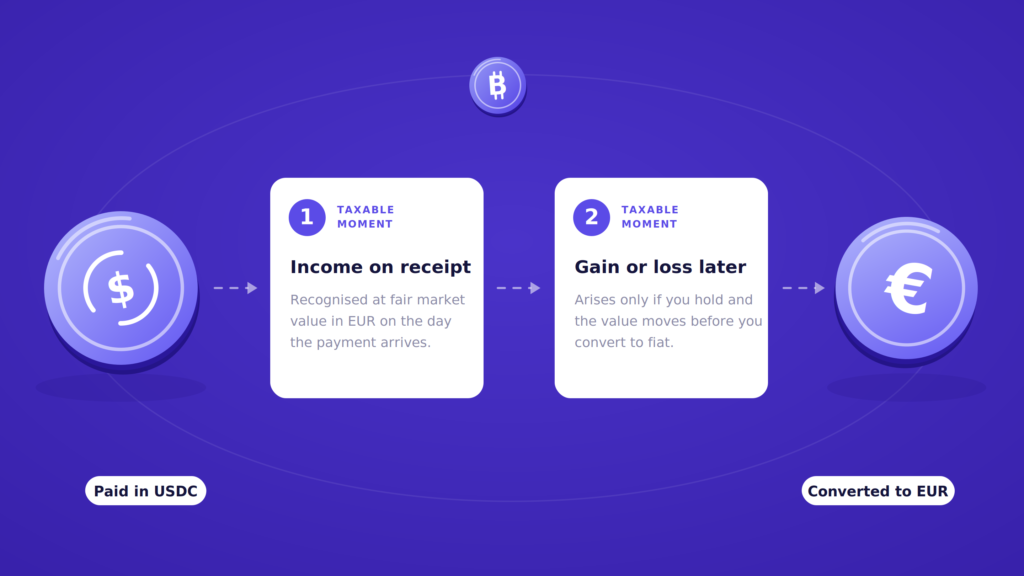

The general principle across most jurisdictions works like this. Crypto received as revenue is recognized as income at its fiat value on the day you receive it. That value becomes your cost basis. If you later sell or convert that crypto at a different value, a separate taxable gain or loss can arise.

Note what this does not do. It doesn’t invent a new accounting treatment. Irish Revenue is explicit that for businesses accepting crypto there is no change to when revenue is recognized or how taxable profits are calculated, and that accounts for tax purposes cannot be prepared in crypto at all. Euro or functional currency, same as always.

So there can be two taxable moments hiding in one crypto payment. First, the income when you receive it. Second, a gain or loss if the crypto’s value moves before you convert it to fiat.

The simplest way to avoid the second one is to convert to fiat on receipt, which removes the holding period entirely. If you hold, you take on the price exposure and the extra accounting that comes with it. We unpack that side in accounting for crypto payments.

How the later gain gets classified, whether it’s a capital gain, trading income, or something FX-like, and at what rate, is genuinely member-state specific. Another advisor conversation.

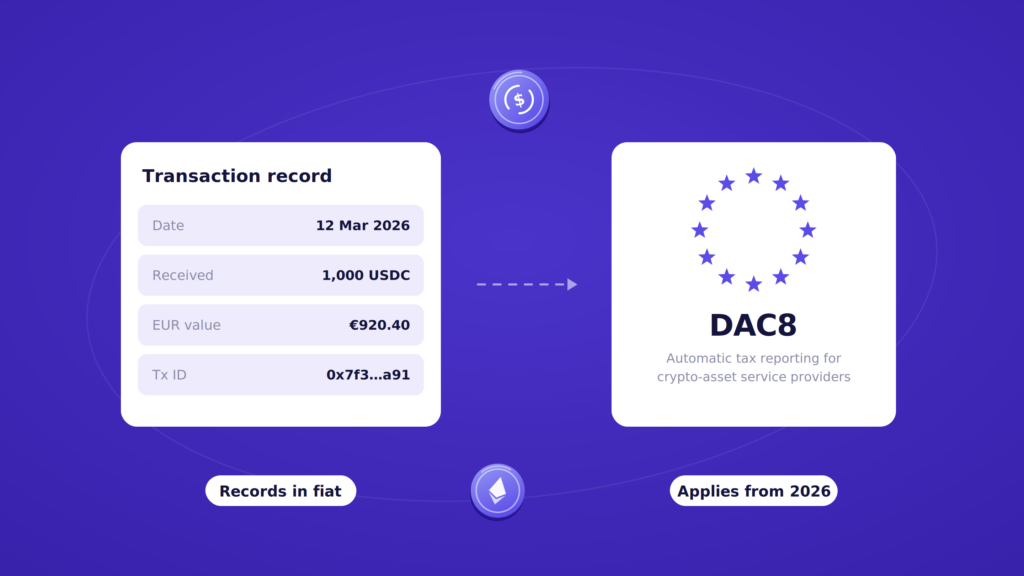

Record-keeping, and why DAC8 makes it non-optional

Whatever the local details, one obligation is universal. You need records of the fiat value of every crypto transaction.

- The date of the transaction

- The crypto amount and the asset

- The fiat-equivalent value

- The exchange rate you used, and where it came from

- Wallet addresses and transaction IDs

This is what lets you report VAT and income correctly, and what you’ll need if anyone ever asks. Retention periods are set nationally rather than by the EU, and they are longer than people assume. Ireland requires six years.

Keeping those records used to be something diligent businesses did quietly. Now the EU is formalizing the visibility around it. DAC8, the EU’s crypto tax-reporting directive, brings crypto-asset service providers into automatic tax reporting. It is Council Directive (EU) 2023/2226, adopted on 17 October 2023, and the rules apply from 1 January 2026. The first reports cover the 2026 year and land with tax authorities in 2027, with member states exchanging the data by 30 September 2027.

DAC8 puts the reporting obligation on the providers, not directly on ordinary merchants. But the practical effect for you is real. Your crypto activity is becoming far more visible to tax authorities, which turns accurate self-reporting from good hygiene into the only sensible option. It also makes your payment provider’s own compliance your problem, which is the argument we make in how MiCA reshapes vendor risk for EU businesses.

How member states actually treat this

The principles above hold, but you can see them applied in national guidance.

Germany. The Federal Ministry of Finance applied Hedqvist directly in its letter of 27 February 2018. Where Bitcoin is used purely as a direct contractual means of payment, its use is treated the same as the use of conventional means of payment, so handing over Bitcoin to settle a bill is not itself a taxable supply. The exchange is exempt. VAT on the underlying sale still applies, and the ministry set out the conversion rule described above.

Ireland. Revenue’s position is that no special tax rules for crypto-asset transactions are required. Normal VAT rules apply to goods and services sold in exchange for crypto, and for a business there’s no change to when income is recognized or how taxable profits are calculated. The crypto is simply valued at its euro equivalent.

Different countries, same spine. Crypto is the payment rail, the tax follows the transaction.

Frequently asked questions

Do I have to charge VAT if a customer pays in crypto?

Yes. If the sale would be subject to VAT when paid in fiat, it’s subject to VAT when paid in crypto. The payment method doesn’t change the VAT treatment of the underlying goods or services.

Is accepting crypto itself a taxable event?

Receiving crypto as payment for a sale is generally recognized as income at its fiat value on the day you receive it. A separate taxable gain or loss can arise later if you hold the crypto and its value changes before you convert it.

What value do I use on the invoice?

The fiat value of the goods or services at the time of the transaction. Authorities generally follow the Article 91(2) approach used for foreign currency, meaning the most recent selling rate or the latest ECB rate when VAT becomes chargeable. The rate source your own tax authority accepts can differ, so confirm the specifics locally and document whichever rate you use.

What records do I need to keep?

Keep the date, crypto amount, fiat-equivalent value, exchange rate used, wallet addresses, and transaction IDs for every crypto payment. These records support your VAT and income tax reporting. Retention periods are national, and six years is a realistic planning assumption.

What is DAC8 and does it affect my business?

DAC8 is Council Directive (EU) 2023/2226, which extends automatic tax reporting to crypto-asset service providers from 1 January 2026. It obligates providers rather than merchants, but it makes crypto activity far more visible to tax authorities, so accurate self-reporting matters more than it did.

The bottom line

Accepting crypto doesn’t move you into some tax-free zone. It moves the payment onto a different rail while the tax stays exactly where it always was, attached to the sale. VAT applies to what you sell. Income is recognized at fiat value on receipt. Records need to exist in euro. And with DAC8, the era of crypto being invisible to tax authorities is ending.

None of this is a reason to avoid crypto payments. It’s a reason to run them cleanly, ideally with a provider that settles to fiat and hands you the transaction records you need. We wrote more about that in how to run a compliant crypto payment operation.

Thinking about accepting crypto without turning your books into a headache? Start with us.

This article is general information and not tax advice. Crypto tax treatment varies by jurisdiction. Consult a qualified local tax advisor before making decisions.

Accept crypto with CoinGate

Accept crypto with confidence using everything you need in one platform.