Accept crypto with CoinGate

Accept crypto with confidence using everything you need in one platform.

Stablecoin Payouts: A Practical Guide for Paying Partners, Affiliates, and Contractors

Ask a finance team why they’re looking into stablecoin payouts and the answer is rarely about technology. It’s usually a person. A top affiliate in Brazil who waited nine days for a wire. A contractor in Nigeria whose bank took a cut on both ends. A partner who finally wrote: “Can you just send USDC?”

Recipients are driving this shift, and they have a point. The question for the business is different though: can you pay people in stablecoins with the same control, approval flow, and paper trail you’d demand from any other payment process?

You can. Here’s how it works in practice.

Think it’s time to introduce cryptocurrency operations to your business? Sign up for CoinGate.

Why stablecoins became the payout asset of choice

Crypto payouts solve the cross-border problem: no correspondent banks, no clearing delays, funds arrive in minutes rather than days. We’ve compared the costs and timelines against SWIFT in detail, and the gap is not subtle.

But paying someone in Bitcoin introduces a new conversation: what if the price moves before they convert it? Stablecoins end that conversation. The recipient gets digital dollars that are worth the same tomorrow. Predictable for them, predictable for your books.

That combination, crypto speed with fiat stability, is why stablecoins dominate the payout side even at businesses that still settle their incoming payments in euros.

Who is switching, and why now

Three groups show up most often in our merchant base:

- Affiliate networks and ad platforms paying hundreds or thousands of publishers monthly. We’ve written about how mass payouts work at that scale, and Coinzilla’s story shows what changes when the process stops being painful.

- Companies with remote teams and contractors spread across countries where bank transfers are slow, expensive, or unreliable. Our freelancer payment guide covers the compliance and tax side of that setup.

- Marketplaces and platforms that owe money to global sellers and need payouts to be a process, not a monthly project.

The common thread: many recipients, many countries, recurring schedule. The more of those boxes you tick, the more the banking rails creak.

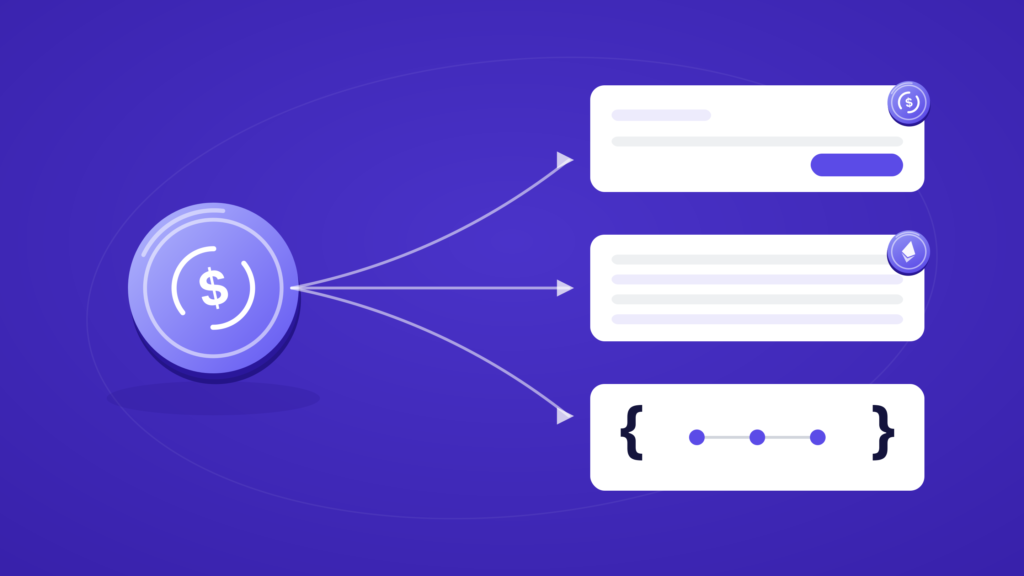

Three payout workflows, from manual to fully automated

A payout system has to match how your team actually operates. We built our payout solution around three workflows for that reason.

One-off payouts from the dashboard

Log in, add a recipient address or pick a saved contact, choose the asset and amount, review, send. No setup, no code. This fits vendors, individual contractors, and anything occasional.

CSV batch payouts

Upload one file with all recipient details and generate the entire batch in seconds, with automatic field validation. This is the workhorse for affiliate settlements and reward runs. Your operations person handles a thousand payouts the way they’d handle ten, and engineering never gets involved.

API payouts with webhooks

For platforms where payouts are part of the product, the API automates the full cycle: create payouts programmatically, monitor every status change through webhooks, reconcile automatically. Set it up once, then let it run.

Most businesses start with the dashboard, move to CSV when volume grows, and reach for the API when payouts become continuous. There’s no wrong entry point.

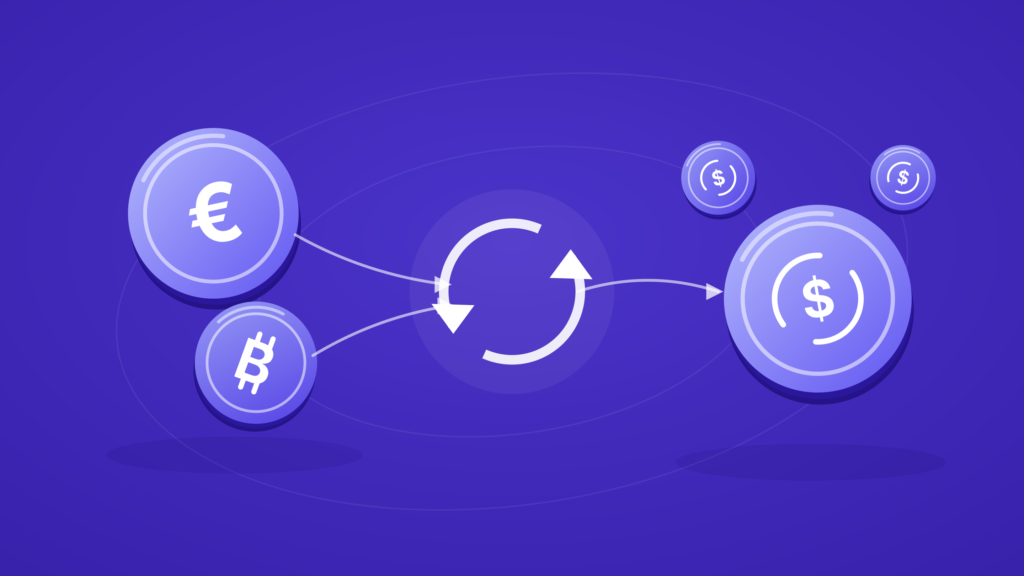

FX conversion: hold one asset, send another

Here’s the capability that quietly removes the most treasury work. You don’t need to hold the asset you’re paying out.

Say your balance sits in EUR, or in BTC that customers paid you. A partner wants USDC. With FX conversion, you create the payout and the conversion happens automatically at the moment of payment. No pre-buying stablecoins, no juggling balances before every payout run, no leftover dust in five currencies.

In practice this means you can keep your treasury policy simple (hold what you prefer) while every recipient gets exactly the asset they asked for. Fewer steps, fewer mistakes, cleaner accounting.

The controls finance teams actually need

This is where “sending crypto” becomes “running payouts.” The difference is governance:

- Four-eye approval. Batch payouts can require a second authorized reviewer before anything moves. One person uploads, another approves.

- Role-based permissions. Define who can view, create, or approve payouts. The intern reconciles, the CFO approves, and the system enforces it.

- Complete records. Every payout carries its TXID, timestamp, fees, asset details, and FX conversion data. Filter and export everything for accounting and audits.

- Account security. MFA and activity logs, so you know who did what and when.

Irreversibility is crypto’s trade-off. You can’t recall a sent payout the way you can sometimes recall a wire. The controls above exist precisely so the mistake never leaves the building.

Compliance questions to settle first

Two things are worth knowing before the first payout run.

First, the sender side carries the compliance weight. Your business account goes through standard KYB checks, and payout operations run under AML requirements. Recipients only need a wallet address that supports the chosen asset and network. No account, no onboarding on their end.

Second, your provider’s regulatory status is now part of your own vendor risk. We operate under a MiCA license from the Bank of Lithuania, and we’ve explained how to run a compliant crypto payment operation if you want the full picture of what that should look like.

Getting started

- Open and verify a business account.

- Deposit funds. Crypto or fiat. FX conversion means either works as a payout source.

- Run one small payout from the dashboard. Learn the flow before you scale it.

- Set permissions and approval rules to match how your team divides responsibility.

- Scale into CSV or API when the volume tells you to.

Pay the way your partners already think

Your best partners are global, and their patience for wire transfers is not. Stablecoin payouts let you pay them at the speed they work, in an asset that holds its value, without giving up the approvals and audit trail your finance team rightly refuses to live without.

The rails are ready. The controls are ready. The only thing still moving at 2015 speed is the wire your partner is waiting on.

Ready to stop explaining SWIFT delays to your partners? Start with us.

Frequently asked questions

Do recipients need a CoinGate account?

No. A compatible wallet address is enough. Funds are sent directly on-chain.

Which assets and networks can I use?

Major cryptocurrencies and stablecoins, including USDC across multiple networks, plus BTC, ETH, LTC, TRX, SOL and more. The full list is here.

Can I send stablecoin payouts if I only hold euros or Bitcoin?

Yes. FX conversion converts your balance into the payout asset at the moment of payment, automatically.

Is there a limit on payout size or volume?

Minimums depend on the asset and network. Limits are built for high-volume operations, and exact figures are visible in the dashboard or via API.

How do I reconcile stablecoin payouts?

Every payout includes TXID, timestamps, fees, and FX data, and full history exports in a few clicks. Your accountant gets consistent records instead of screenshots.

Accept crypto with CoinGate

Accept crypto with confidence using everything you need in one platform.